Building a better budget

Creating, managing and tracking your dealership’s financials

You probably got into the boating industry because it was fun and you wanted to enjoy your job. But you also probably did so with the assumption that you would be making money. So while budgeting may not be the most exciting part of running your dealership, it is without a doubt one that needs your devoted attention.

But where should a dealer start? For one, the very first thing a dealership needs to have are good, clean financial statements. If you don’t know what your cash and financials look like, it can be incredibly time consuming and expensive to fix mistakes down the road.

“You need to have good financial statements to make good use of a budget process. You need a good financial foundation of managing your cash and financials to have a budget and have any use from it,” otherwise you’re just running blind, said Andreas Majewski, controller of Lake Union Sea Ray.

A way to guarantee this is to hire an accountant or bookkeeper in-house. Majewski is a CPA and an MBA, and his full-time job is to manage Lake Union Sea Ray’s budget. This has been beneficial because most managers are bogged down with the hectic atmosphere of running the dealership and they don’t always have the ability to focus on the numbers.

“They’re just so busy trying to do their jobs and sell and work with the public that they don’t necessarily have the time or the motivation to really drill down into their details,” said Majewski. “They’ve got a good organic idea of how the month’s going … but I’ve got a little bit more of a luxury of [having time to] delve into it a little bit deeper. Specialization is what it comes down to.”

There are several tools available if the task of building a budget seems daunting. Companies like Parker Business Planning and Spader Business Management offer online budgeting programs that allow dealers to plug in numbers for every line item of a dealer’s financials and create detailed budgets seamlessly. These programs help calculate your net profit, gross margins and more without having to

do complicated work.

“Tracking it is just as easy as dropping your monthly balance into the system each month and it pulls a variance report,” said David Parker, president of Parker Business Consulting, of his online budgeting program. “There’s a one-page summary and then the details behind it for every line item. We track that month- and year-to-date.”

Dealers also use marine management systems like IDS as a main budgetary collection tool and tracking system.

“I think that it really helps us react and to adjust the way we’re managing on an almost daily basis. It gives us a guide on what we should be doing [and] focusing on,” said John Jay Irwin, vice president and parts & accessories director of Irwin Marine.

(Find a list of budgeting resources on p. 36)

Planning out your year

Dealers should begin planning for the upcoming fiscal year a couple months before the current fiscal year-end, whether year-end is a calendar or non-calendar fiscal year.

“It gives us some runway for the inevitable delays that will happen: people traveling and those kinds of things. By the time we really get a preliminary budget together, it could be mid-November by then. It gives us more planning time and time for contingencies,” said Majewski.

The owners and accountants, if you have them, should work together to create a budget, but it is also important to involve the managers of all departments across the dealership. Handing these managers numbers at the beginning of the year that they didn’t have any part in creating allows them to deflect if those numbers aren’t met.

“They’re intimately involved in their business and you want their buy-in in the creation of that budget. You want them to own those numbers they’re coming up with,” said Parker.

“It would be a lot easier just to sit down and have the general manager come up with a budget, but it wouldn’t mean anything unless you share that and have people totally involved in that whole process,” added Irwin.

Start with last year’s actuals to create the budget and manage every number month to month. This acts as your base point, which gives you more confidence in projecting for the next year. It is also beneficial to look at monthly trends to help create a cohesive budget for the upcoming fiscal year. Irwin Marine often looks at monthly trends in a period of three or five years. Developing sales trends by month makes it easy for dealers to use those trends to project next year’s sales.

“We were introduced to that by Spader a long time ago, and really taking a look at it on a yearly [basis] gives you a little bit of inaccuracy. But having three years trending really gives you a big advantage,” said Irwin. “What we wind up with at the end of the year has been pretty close almost down to the last dollar. It’s pretty amazing how that works out.”

This is useful particularly in the seasonality of a boat business, as creating your monthly budget is not as simple as taking your yearly sales and dividing by 12.

“If you take and average your monthly sales – in other words, the month of January is [for example] 2.5 percent – if you will average the dollar amounts by month as a percentage of the total, you can total those up for three to five years and get a really solid amount for each month as to what your monthly sales trends will be for that department,” Parker said. “And then you add it up and do it for the whole company as well.”

Majewski is a bit unique in that he keeps up to 10 years of data. This could come from his accounting experience, but he says it also stems from what he has learned about the boating industry.

“What I’ve learned about this industry is it seems to run in long-term, up-and-down cycles,” he said. Pre-recession, the industry was doing a great job and when the recession did hit, many dealers bottomed out. However, in the past few years dealers have started to make a comeback.

“Now we find it almost useful to look at what we were doing pre-recession again to [ask] are we seeing the same kind of margins we see in a good market? We know we’re doing better than at the bottom of the recession [but] that’s not our benchmark,” said Majewski. “We want to know how do we do when we are really doing well?”

Track, track, track

At minimum, dealers should be tracking their budget monthly. In fact, in some cases, dealers can track budgets more often, such as for unit sales and the sales of labor. Dealers can take a weekly budget for unit sales and build it into the agenda of weekly sales meetings to track how well the departments are doing. That being said, dealers should not spend too much time worrying about the budget while they are tracking it. Irwin takes advice from Spader to “look at the budget monthly, but worry about it quarterly.”

“Until we get into [the end of the quarter], we don’t really start sweating it unless we’re way off. You look at [the budget] but you have to look at it with some educated eyes and knowing where you’re going to be off a little bit,” Irwin said. “We get into October and October’s a little bit off, you worry about it but you know ‘Well, that’s October,’ and there could be some variances. Looking at it at different times of the year with more emphasis [and] looking at it as an overall view, is really important: knowing when to sweat it and when to just watch it. It’s definitely a management tool.”

At Lake Union Sea Ray, all line managers are watching how they are doing compared to the budget, but the drilling down into the minutia of the numbers rests of Majewski’s shoulders.

“Ideally, the month will close, I’ll get most of the expenses put in place so I can say we’re close enough now to look at it. The managers will look at it, I’ll start drawing some conclusions and then they are these things where I’ll do some research and ask [questions], and conversely they might come back and say [with their own questions],” said Majewski. “So it’s a two-way street. I’m asking questions to the people that run the revenue centers and they often will ask me to drill down into expenses that they can’t figure out or see.”

20 groups make budgeting easier

For dealers who are a part of a 20 group, it comes as no surprise to hear that being a 20 group member can exponentially improve how you create, manage and review a budget. The non-competing dealers in these groups have the opportunity to learn from one another’s budgeting processes and see how one dealer is getting five points more for the same boats they’re selling.

“Then you find out the system or process they’re using in order to be able to get those higher margins. Many times it’s just asking for it,” said Parker. “It’s that outside influence that can explain to [dealers] how others are doing [budgeting] and doing better than [they] are in [certain] areas. It gives them the ability to change their system. You change the system, you’ll change your financials.”

Irwin Marine is part of Spader 20 groups, which meet for three days three times a year, and 1.5 days of that time is spent reviewing everyone’s numbers, looking at trends and making comparisons.

“Different people in the group will come up with different ways to look at things,” said Irwin. “It gives you all kinds of perspectives: what your expense ratios are for employees, what you should be spending for each department and for each account, [etc.].”

Top money mistakes

Managing financials can be tricky and there are several mistakes a small business owner in any industry makes. These mistakes could have a small impact or inflict a fatal blow to a business. Here are some of the most common mistakes among small business owners and how to avoid them.

• Not having enough cash reserves. Small businesses often overestimate how quickly they will make a profit and underestimate the expenses attributed to running a business. Make sure you always have a steady base of operating cash.

• Mixing business and personal funds. This is a recipe for disaster, and it is all too common for small businesses to do. Keeping track of how much money the business is actually making or losing becomes increasingly difficult if you use your business credit to pay for a personal purchase and vice versa. Even if it seems like a good idea at the time, keep those entities entirely separate. You’ll have cleaner books because of it.

• Keeping insufficient records. Speaking of the books, one of the biggest mistakes small businesses make is to not stay on top of recordkeeping. Make sure you are tracking you budget as regularly as possible.

• Not reinvesting in the business through hires. The old adage of “you need to spend money to make money” rings true for small businesses. Particularly when it comes to new hires and wanting to hire the best, you get what you pay for.

• Being dependent on credit cards. Whether through a small business loan, a capital infusion or your own funding, get out of credit card debt and build sufficient operating capital.

• Not seeking credit on time. The worst time to ask for a line of credit is when you need it the most. Seek funding when your business is solid and healthy, which is when you will have the most bargaining power to convince a lender you will be able to repay.

• Poor risk management. Always be prepared for the worst-case scenario by protecting all of your assets, including space, equipment and all key employees, including yourself. This means budgeting for and buying adequate property and casualty, liability, disability

and life insurance.

• Shorting yourself on compensation. While it seems like a good decision in the early stages to redistribute profits back into your business, not compensating yourself along the way will harm your personal finances and long-term financial good standing.

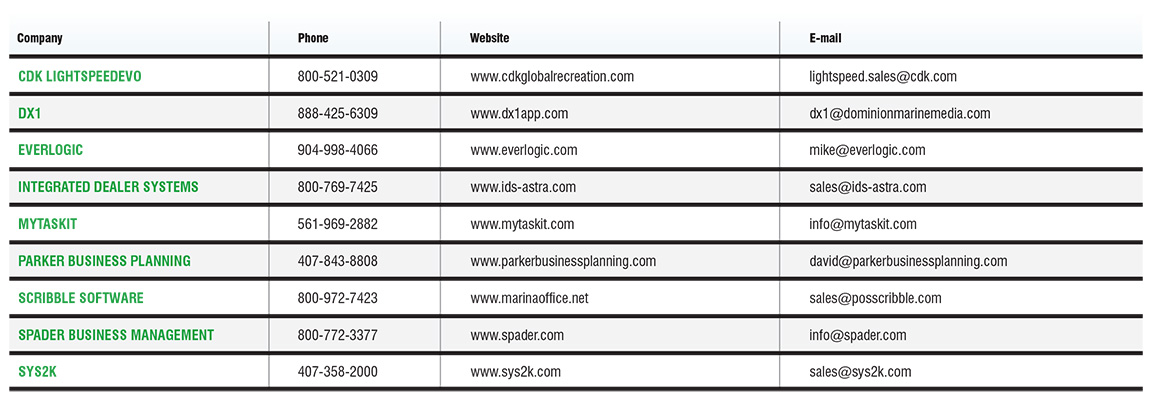

Budgeting resources

Below is a list of marine budgeting and accounting software for dealers.